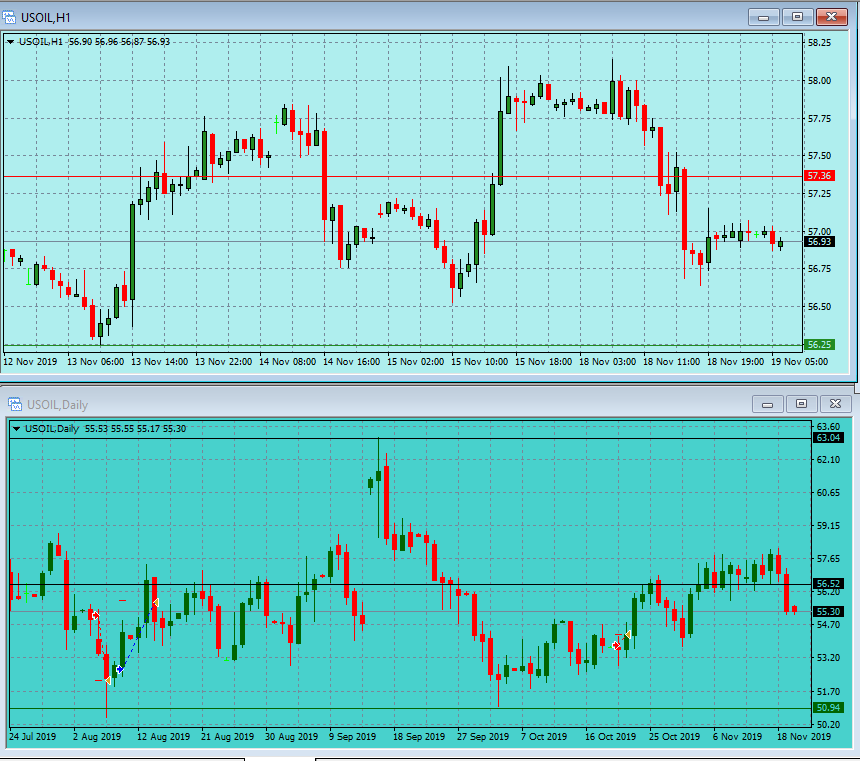

The dollar mostly sideways yesterday awaiting the release of the FOMC meeting minutes today in the afternoon and more on the Brexit and the US China trade deal. Overnight Asian equity markets traded lower after US President Trump harsh rhetoric on China regarding the trade deal, stating more US tariffs if the parties are unable to strike a deal. Dec 15 is the target date for more US tariffs if an agreement is not reached by then. The JPY, CHF and Metals traded higher on the news as investors switch some positions back to “safe heavens”. EU and US futures also traded lower on the news overnight. Gold closed higher at $1,472 per ounce yesterday and Silver closed higher as well, at $17.1 per ounce. Oil was the big loser in the markets yesterday, taking a 3.3% dive on global growth concerns, and big 6 million barrels increase in US inventories posted by the API and news that Russia is unlikely to go ahead with the OPEC proposed production cuts when the parties will meet in 2 weeks in Vienna. Oil closed lower 4.3% over the past 2 sessions, closing at $55.21 per barrel yesterday, ahead of US Inventories set to be released at 10:30 am US today.

CAD CPI at 1:30 pm, Oil inventories at 3:30 pm and the FOMC Meeting minutes at 6:00 pm are the important news on the agenda Wednesday. (all times GMT).

| Global Markets 24 hours wrap-up | ||||||

|---|---|---|---|---|---|---|

| Market | GBPUSD | USDJPY | EURJPY | EURUSD | GOLD | OIL |

| 19.10.19 | -0.22% | -0.11% | -0.04% | 0.08% | 0.11% | -3.24% |

| USDMXN | USDCHF | AUDUSD | AUDJPY | USDCAD | Silver | Nat Gas |

| 0.22% | 0.1% | 0.25% | 0.14% | 0.43% | 0.55% | -2.14% |

| Dollar Index | DAX | FTSE100 | CAC40 | EURSXX50 | NIKKEI225 | CSI300 |

| 0.04% | 0.11% | 0.22% | -0.35% | -0.23% | -0.62% | -0.64% |

| 1 YEAR | 17.47% | 5.41% | 19.98% | 18.63% | 7.25% | 22.17% |

| Swing report | ||||||

|---|---|---|---|---|---|---|

| TRADE | ENTRY PRICE | POSITION | OPEN PROFIT | DATE TRIGGERED | STOP LOSS | UPDATES |

| EURSX50 | 3670 | 8 | 140 | 5/11 | 3670 | |

| GBPUSD | 2963 | -512 | 19/11 | 2960 | stopped out | |

| OPEN PROFIT | $140 | |||||

Oil traded sharply lower yesterday on global growth and production worries ahead of the Inventories numbers today at 10:30 am US.

DAX futures weaker this morning and Gold trading higher after US president Trump harsh rhetoric on China overnight.

Warning: The information provided on this page (“the information”) is for instructional purposes only, for enhancing your general knowledge of the capital market in general and using trading methods and the technical analysis method in particular. We hereby clarify that the company, its management, staff, shareholders and agents do not hold investment advisor licenses and/or portfolio manager licenses by any applicable law, and do not pretend to advise any person on the worthiness of buying, selling, holding or investing in securities and other financial assets. The information should not be construed to be a recommendation or opinion, and any person who makes any decision based on the information – does so entirely at their own risk. Be aware that the information cannot serve in lieu of advice which accounts for specific information and needs of an individual, and that investing in securities and financial assets may cause loss. The company, its management, staff and agents may have a personal interest in issues related to the information, and may hold specific securities mentioned in the information, or similar securities. If you use the information, you waive any claim or demand against the company or anyone acting on its behalf.